City and Regional Reports from the

California Public Banking Alliance

We’re making significant headway in public banking, with various local governments across California showing their commitment by providing funding for public bank viability studies and business plans. These efforts are aimed at outlining the implementation path for the establishment of local public banks in their respective areas.

Read our press in Next City: Public Banking Efforts Are Gaining Momentum And Clarity In California. From Los Angeles to the Central Coast, from San Francisco to the East Bay and Sacramento, major public banking plans are emerging from California cities.

Also, be on the lookout for our new video introduction to public banking! We’ll share the link to “You Can Public Bank on That” soon!

CENTRAL COAST

People for Public Banking Central Coast has been advocating since 2019 for a regional public bank to encompass the counties of Santa Cruz, Santa Barbara, Monterey, and San Luis Obispo, including the cities within those counties. Currently, 12 jurisdictions have formally expressed interest in participating in a viability study to create the bank, including Santa Barbara County which has pledged $25,000 toward the study.

A possible first step will be to create a municipal finance corporation or green bank which could be called the Central Coast People’s Fund. We continue to focus on education and outreach, especially to city managers and finance directors. We also hope to educate large numbers of citizens on the benefits of public bank financing for projects like affordable housing and disaster mitigation.

EAST BAY

Public Bank East Bay is planning a suite of announcements of important milestones in mid-September. While we prepare those announcements, we (including our slate of Bank Board candidates) are very busy refining our draft business plan and charter application, collaborating closely with Alameda County and the three cities of Berkeley, Oakland, and Richmond so they will be ready to sign that application and contribute capital to the bank, and providing comprehensive training for our Bank Board candidates. We’re actively reaching out to local financial institutions as potential partners under AB 857 and are thrilled to announce recent foundation grants of $300,000 from the Irvine Foundation and an additional $150,000 grant (to be shared with Rise Economy). These grants will greatly support our research and outreach efforts for public banking.

LOS ANGELES

In June 2023, the Los Angeles City Council unanimously approved $460,000 to fund Phase 1 of the public bank feasibility study and business plan. Public Bank LA is collaborating with coalition leaders including SEIU 721 to secure an additional $240,000 to support Phase 2. Public Bank LA is also engaging LA County Supervisors working alongside Move LA and Destination Crenshaw on the LA County Regional Public Bank in an effort that runs parallel to the LA City Public Bank.

The Jain Family Institute and the Berggruen Institute released the full LA public bank report series including five extensive briefings covering: a series introduction, affordable housing, democratic frameworks, clean energy portfolio options, interactive balance sheet simulator, and financial justice portfolio options. The 160-page report series provides the most comprehensive analysis of a public bank within the movement to date.

Recent LA coverage:

Los Angeles Times

California Globe

CBS News

POMONA VALLEY

In addition to a presentation at a local Rotary Club and University Club, Public Bank Pomona Valley’s leadership met with Public Banking Institute founder, Ellen Brown, to discuss the history and national prospects of the movement. We plan to meet soon with the Claremont Democratic Club as well as a gathering organized by the Human Values Institute, which is working with several groups promoting economic well-being in the Pomona region.

The Public Bank Pomona Valley advocacy group includes several current and former elected officials in city government, as well as community leaders of nonprofits and foundations promoting economic justice issues. While grassroots education is our primary task for now, we are ready to urge our Pomona Valley cities to begin developing their banking business plan when the time is right.

SACRAMENTO

A unanimous vote from the Banking and Audit Committee of the City Council of Sacramento was obtained this past spring authorizing up to $250,000 for a viability study and business plan for a Public Bank. The Committee is made up of the Mayor of Sacramento as well as 3 council members. City staff in the office of the Treasurer of Sacramento are now working on a draft RFP for a Viability Study with support from the Sacramento Public Bank Working Group. The Sacramento Public Bank Working Group continues to educate the public on the advantages of a Public Bank and has met with the City Treasurer and Banking Manager.

SAN FRANCISCO

The SF Public Bank Coalition (SFPBC) is mobilizing supporters for the presentation of the Reinvest In SF Working Group public banking plan to the Board of Supervisors on September 5, 2023. SF Public Bank is also working to establish a “Green Bank” to gain access to Greenhouse Gas Reduction funds.

On August 31, SF Public Bank will have its first general membership meeting open to all interested in joining our coalition. We presented to the Loma Prieta Sierra Club which sees public banking in the Peninsula and Silicon Valley as a means of financing innovative climate crisis interventions. We are hoping this helps reinvigorate the South Bay chapter of the California Public Banking Alliance.

Recent SF coverage:

Westside Observer

San Francisco Chronicle

San Francisco Examiner

CALIFORNIA REGIONS

In regions across California, including Pomona Valley and North Coast, our CA Public Banking Alliance teams continue to dedicate themselves to community education and engagement.

We are actively reaching out to public banking advocates in regions that have not yet established CPBA chapters. If you are interested in learning more about getting public banking started in your area, or know someone who might be, please contact our outreach coordinator, David Cobb at davidkcobb@gmail.com. Below is a list of areas we are especially hoping to form chapters of public bank supporters.

BAKERSFIELD

FRESNO

HUMBOLDT / NORTH COAST

RIVERSIDE / SAN BERNARDINO

SAN DIEGO

SANTA ROSA / SONOMA COUNTY

SOUTH BAY / SILICON VALLEY

STOCKTON / MODESTO

CALACCOUNT

Our universal banking program, CalAccount (AB 1177), is an ongoing initiative of the CPBA. Along with coalition partners SEIU California and Rise Economy, we’re tracking the progress of the CalAccount program in the monthly hearings for community representation on the CalAccount advisory board and ensuring the program’s successful implementation. Establishing positive relationships with regulatory authorities is vital; we’re actively building partnerships with the California Department of Financial Protection and Innovation agency (DFPI), including DFPI Commissioner Cloey Hewlett.

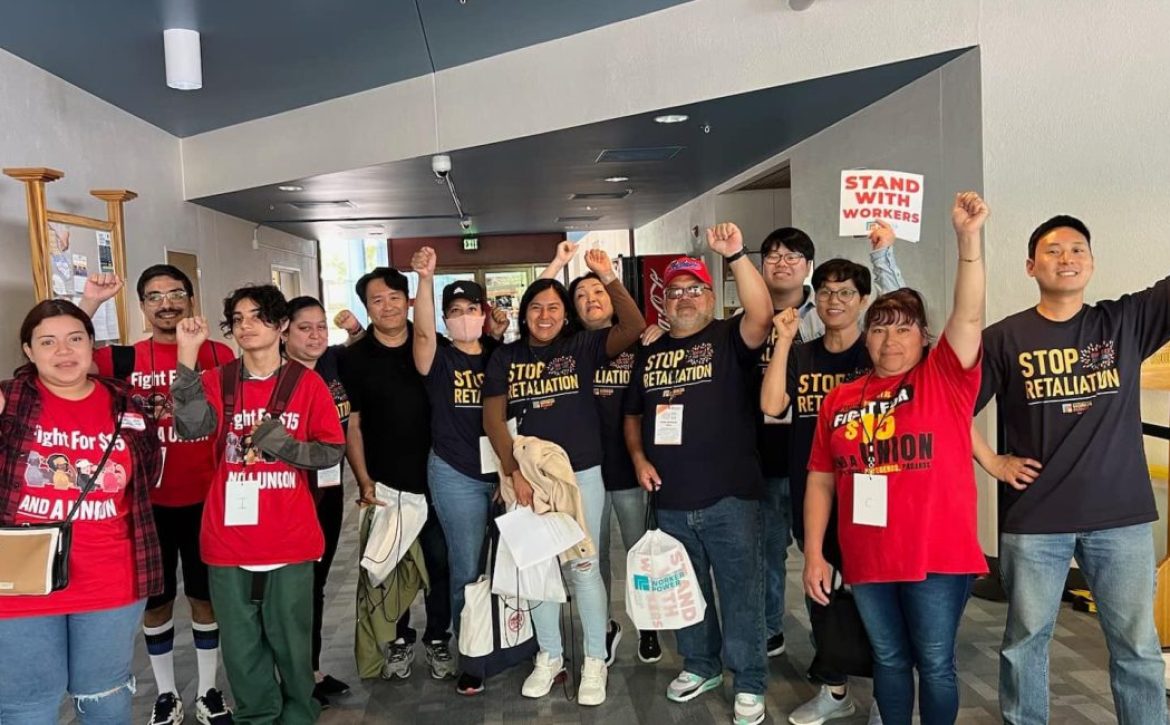

People power in Sacramento! Fight for $15 and KIWA, Koreatown Immigrant Workers Alliance workers turned out in support of CalAccount, urging the State Treasurer Fiona Ma and Commissioners to incorporate community input, a crucial step to ensure the program’s success and provide essential banking services for nearly 10 million low-wage Californians.

Read the CalAccount August Legislative Briefing.

FEDERAL PUBLIC BANKING ACT

The CPBA is currently advising Congresswoman Rashida Tlaib’s office, providing insights for the amendments in preparation for the federal Public Banking Act‘s reintroduction, anticipated in the coming months, spearheaded by Representatives Tlaib and Ocasio-Cortez.